This post shows how to work with negative binomial distribution from an actuarial modeling perspective. The negative binomial distribution is introduced as a Poisson-gamma mixture. Then other versions of the negative binomial distribution follow. Specific attention is paid to the thought processes that facilitate calculation involving negative binomial distribution.

Negative Binomial Distribution as a Poisson-Gamma Mixture

Here’s the setting for the Poisson-gamma mixture. Suppose that

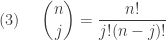

![\displaystyle (1) \ \ \ \ P[X=k]=\frac{\Gamma(\alpha+k)}{k! \ \Gamma(\alpha)} \ \biggl( \frac{\rho}{1+\rho} \biggr)^\alpha \ \biggl(\frac{1}{1+\rho} \biggr)^k \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%281%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3D%5Cfrac%7B%5CGamma%28%5Calpha%2Bk%29%7D%7Bk%21+%5C+%5CGamma%28%5Calpha%29%7D+%5C+%5Cbiggl%28+%5Cfrac%7B%5Crho%7D%7B1%2B%5Crho%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Crho%7D+%5Cbiggr%29%5Ek+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

The distribution described in (1) is one parametrization of the negative binomial distribution (derived here). It has two parameters

![\displaystyle (2) \ \ \ \ P[X=k]=\frac{\Gamma(\alpha+k)}{k! \ \Gamma(\alpha)} \ \biggl( \frac{1}{1+\theta} \biggr)^\alpha \ \biggl(\frac{\theta}{1+\theta} \biggr)^k \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%282%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3D%5Cfrac%7B%5CGamma%28%5Calpha%2Bk%29%7D%7Bk%21+%5C+%5CGamma%28%5Calpha%29%7D+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5Ek+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

The distribution described in (2) is obtained when the gamma mixing weight

Both (1) and (2) contain the ratio

The Poisson-gamma mixture is discussed in this blog post in a companion blog called Topics in Actuarial Modeling.

General Binomial Coefficient

The familiar binomial coefficient is the following:

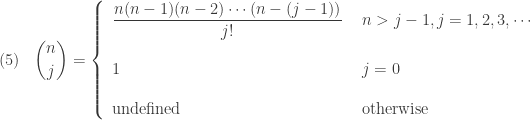

where the top number

The expression in (4) is obtained by canceling out

Thus the expression in (4) gives a new meaning to the binomial coefficient where

For example,

We now use the binomial coefficient defined in (5) to simplify the ratio

The right hand side of the above expression is precisely the binomial coefficient

where

Negative Binomial Distribution

With relation (6), the two versions of Poisson-gamma mixture stated in (1) and (2) are restated as follows:

![\displaystyle (7) \ \ \ \ P[X=k]=\binom{\alpha+k-1}{k} \ \biggl( \frac{\rho}{1+\rho} \biggr)^\alpha \ \biggl(\frac{1}{1+\rho} \biggr)^k \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%287%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3D%5Cbinom%7B%5Calpha%2Bk-1%7D%7Bk%7D+%5C+%5Cbiggl%28+%5Cfrac%7B%5Crho%7D%7B1%2B%5Crho%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Crho%7D+%5Cbiggr%29%5Ek+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

![\displaystyle (8) \ \ \ \ P[X=k]=\binom{\alpha+k-1}{k} \ \biggl( \frac{1}{1+\theta} \biggr)^\alpha \ \biggl(\frac{\theta}{1+\theta} \biggr)^k \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%288%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3D%5Cbinom%7B%5Calpha%2Bk-1%7D%7Bk%7D+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5Ek+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

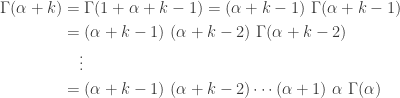

The above two parametrizations of negative binomial distribution are used if information about the Poisson-gamma mixture is known. In (7), the gamma distribution in the Poisson-gamma mixture has shape parameter

![\displaystyle (9) \ \ \ \ P[X=k]=\binom{\alpha+k-1}{k} \ p^\alpha \ (1-p)^k \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%289%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3D%5Cbinom%7B%5Calpha%2Bk-1%7D%7Bk%7D+%5C+p%5E%5Calpha+%5C+%281-p%29%5Ek+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

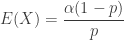

In (9), the negative binomial distribution has two parameters

![\displaystyle \begin{aligned} (10) \ \ \ \ P[X=k]&=\binom{\alpha+k-1}{k} \ p^\alpha \ (1-p)^k \\&=\frac{(\alpha+k-1)!}{k! \ (\alpha-1)!} \ p^\alpha \ (1-p)^k \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ k=0,1,2,3,\cdots \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+%2810%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%26%3D%5Cbinom%7B%5Calpha%2Bk-1%7D%7Bk%7D+%5C+p%5E%5Calpha+%5C+%281-p%29%5Ek+%5C%5C%26%3D%5Cfrac%7B%28%5Calpha%2Bk-1%29%21%7D%7Bk%21+%5C+%28%5Calpha-1%29%21%7D+%5C+p%5E%5Calpha+%5C+%281-p%29%5Ek+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots+%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

In version (10), the parameters are

Version (10) has a natural interpretation. A Bernoulli trial is an random experiment that results in two distinct outcome – success or failure. Suppose that the probability of success is

A special case of (10). When the parameter

![\displaystyle (11) \ \ \ \ P[X=k]=p \ (1-p)^k \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ \ k=0,1,2,3,\cdots](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%2811%29+%5C+%5C+%5C+%5C+P%5BX%3Dk%5D%3Dp+%5C+%281-p%29%5Ek+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+%5C+k%3D0%2C1%2C2%2C3%2C%5Ccdots&bg=ffffff&fg=333333&s=0&c=20201002)

The distribution in (11) is said to be a geometric distribution with parameter ![P[X>k]=(1-p)^{k+1}](https://s0.wp.com/latex.php?latex=P%5BX%3Ek%5D%3D%281-p%29%5E%7Bk%2B1%7D&bg=ffffff&fg=333333&s=0&c=20201002)

More about Negative Binomial Distribution

The probability functions of various versions of the negative binomial distribution have been developed in (1), (2), (7), (8), (9), (10) and (11). Other distributional quantities can be derived from the Poisson-gamma mixture. We derive the mean and variance of the negative binomial distribution.

Suppose that the negative binomial distribution is that of version (8). The conditional random variable

The following derives the mean and variance of

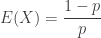

![E(X)=E[E(X \lvert \Lambda)]=E[\Lambda]=\alpha \theta](https://s0.wp.com/latex.php?latex=E%28X%29%3DE%5BE%28X+%5Clvert+%5CLambda%29%5D%3DE%5B%5CLambda%5D%3D%5Calpha+%5Ctheta&bg=ffffff&fg=333333&s=0&c=20201002)

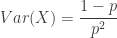

![\displaystyle \begin{aligned} Var(X)&=E[Var(X \lvert \Lambda)]+Var[E(X \lvert \Lambda)] \\&=E[\Lambda]+Var[\Lambda] \\&=\alpha \theta+\alpha \theta^2 \\&=\alpha \theta (1+\theta) \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+Var%28X%29%26%3DE%5BVar%28X+%5Clvert+%5CLambda%29%5D%2BVar%5BE%28X+%5Clvert+%5CLambda%29%5D+%5C%5C%26%3DE%5B%5CLambda%5D%2BVar%5B%5CLambda%5D+%5C%5C%26%3D%5Calpha+%5Ctheta%2B%5Calpha+%5Ctheta%5E2+%5C%5C%26%3D%5Calpha+%5Ctheta+%281%2B%5Ctheta%29++%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

The above mean and variance are for parametrization in (8). To obtain the mean and variance for the other parametrizations, make the necessary translation. For example, to get (7), plug

| Version | Mean | Variance |

|---|---|---|

| (7) |  |

|

| (8) |  |

|

| (9) and (10) |  |

|

| (11) |  |

|

The table shows that the variance of the negative binomial distribution is greater than its mean (regardless of the version). This stands in contrast with the Poisson distribution whose mean and the variance are equal. Thus the negative binomial distribution would be a suitable model in situations where the variability of the empirical data is greater than the sample mean.

Modeling Claim Count

The negative binomial distribution is a discrete probability distribution that takes on the non-negative integers

The Poisson-gamma model has a great deal of flexibility. Consider a large population of individual insureds. The number of losses (or claims) in a year for each insured has a Poisson distribution with mean

Thus in a Poisson-gamma model, the claim frequency for an individual in the population follows a Poisson distribution with unknown gamma mean. The weighted average of these conditional Poisson claim frequencies is a negative binomial distribution. Thus the average claim frequency over all individuals has a negative binomial distribution.

The table in the preceding section shows that the variance of the negative binomial distribution is greater than the mean. This is in contrast to the fact that the variance and the mean of a Poisson distribution are equal. Thus the unconditional claim frequency

We present two examples. More examples to come at the end of the post.

Example 1

For a given insured driver in a large portfolio of insured drivers, the number of collision claims in a year has a Poisson distribution with mean

- what is the probability of having exactly 2 collision claims in the next year?

- what is the probability of having at most one collision claim in the next year?

The number of collision claims in a year is a Poisson-gamma mixture and thus is a negative binomial distribution. From the given gamma mean and variance, we can determine the parameters of the gamma distribution. In this example, we use the parametrization of (8). Expressing the gamma mean and variance in terms of the shape and scale parameters, we have

![\displaystyle P[X=0]=\biggl( \frac{1}{21} \biggr)^{0.2}=0.5439](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+P%5BX%3D0%5D%3D%5Cbiggl%28+%5Cfrac%7B1%7D%7B21%7D+%5Cbiggr%29%5E%7B0.2%7D%3D0.5439&bg=ffffff&fg=333333&s=0&c=20201002)

![\displaystyle P[X=1]=\binom{0.2}{1} \ \biggl( \frac{1}{21} \biggr)^{0.2} \ \biggl( \frac{20}{21} \biggr)=0.2 \ \biggl( \frac{1}{21} \biggr)^{0.2} \ \biggl( \frac{20}{21} \biggr)=0.1036](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+P%5BX%3D1%5D%3D%5Cbinom%7B0.2%7D%7B1%7D+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B21%7D+%5Cbiggr%29%5E%7B0.2%7D+%5C+%5Cbiggl%28+%5Cfrac%7B20%7D%7B21%7D+%5Cbiggr%29%3D0.2+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B21%7D+%5Cbiggr%29%5E%7B0.2%7D+%5C+%5Cbiggl%28+%5Cfrac%7B20%7D%7B21%7D+%5Cbiggr%29%3D0.1036&bg=ffffff&fg=333333&s=0&c=20201002)

![\displaystyle P[X=2]=\binom{1.2}{2} \ \biggl( \frac{1}{21} \biggr)^{0.2} \ \biggl( \frac{20}{21} \biggr)^2=\frac{1.2 (0.2)}{2!} \ \biggl( \frac{1}{21} \biggr)^{0.2} \ \biggl( \frac{20}{21} \biggr)^2=0.0592](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+P%5BX%3D2%5D%3D%5Cbinom%7B1.2%7D%7B2%7D+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B21%7D+%5Cbiggr%29%5E%7B0.2%7D+%5C+%5Cbiggl%28+%5Cfrac%7B20%7D%7B21%7D+%5Cbiggr%29%5E2%3D%5Cfrac%7B1.2+%280.2%29%7D%7B2%21%7D+%5C+%5Cbiggl%28+%5Cfrac%7B1%7D%7B21%7D+%5Cbiggr%29%5E%7B0.2%7D+%5C+%5Cbiggl%28+%5Cfrac%7B20%7D%7B21%7D+%5Cbiggr%29%5E2%3D0.0592&bg=ffffff&fg=333333&s=0&c=20201002)

The answer for the first question is ![P[X=2]=0.0592](https://s0.wp.com/latex.php?latex=P%5BX%3D2%5D%3D0.0592&bg=ffffff&fg=333333&s=0&c=20201002)

![P[X \le 1]=P[X=0]+P[X=1]=0.6475](https://s0.wp.com/latex.php?latex=P%5BX+%5Cle+1%5D%3DP%5BX%3D0%5D%2BP%5BX%3D1%5D%3D0.6475&bg=ffffff&fg=333333&s=0&c=20201002)

Example 2

For an automobile insurance company, the distribution of the annual number of claims for a policyholder chosen at random is modeled by a negative binomial distribution that is a Poisson-gamma mixture. The gamma distribution in the mixture has a shape parameters of

Since the gamma shape parameter is 1, the unconditional number of claims in a year is a geometric distribution with parameter

![\displaystyle P[X>2]=\biggl( \frac{1}{4} \biggr) \ \biggl( \frac{3}{4} \biggr)^3=\frac{27}{256}=0.1055](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+P%5BX%3E2%5D%3D%5Cbiggl%28+%5Cfrac%7B1%7D%7B4%7D+%5Cbiggr%29+%5C+%5Cbiggl%28+%5Cfrac%7B3%7D%7B4%7D+%5Cbiggr%29%5E3%3D%5Cfrac%7B27%7D%7B256%7D%3D0.1055&bg=ffffff&fg=333333&s=0&c=20201002)

A Recursive Formula

The probability functions described in (1), (2), (7), (8), (9), (10) and (11) describe clearly how the negative binomial probabilities are calculated based on the two given parameters. The probabilities can also be calculated recursively. Let ![P_k=P[X=k]](https://s0.wp.com/latex.php?latex=P_k%3DP%5BX%3Dk%5D&bg=ffffff&fg=333333&s=0&c=20201002)

In (12), the numbers

We show that the negative binomial distribution is a member of the (a,b,0) class of distributions. First, assume that the negative binomial distribution conforms to the parametrization in (8) with parameters

Let the initial probability be

![\displaystyle \begin{aligned} P_1&=(a+b) P_0 \\&=\biggl(\frac{\theta}{1+\theta}+ \frac{(\alpha-1) \theta}{1+\theta} \biggr) \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \\&=\alpha \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \frac{\theta}{1+\theta} \\&=\binom{\alpha}{1} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \frac{\theta}{1+\theta}=P[X=1] \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+P_1%26%3D%28a%2Bb%29+P_0+%5C%5C%26%3D%5Cbiggl%28%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D%2B+%5Cfrac%7B%28%5Calpha-1%29+%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C%5C%26%3D%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5C%5C%26%3D%5Cbinom%7B%5Calpha%7D%7B1%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D%3DP%5BX%3D1%5D++%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

![\displaystyle \begin{aligned} P_2&=\biggl(a+\frac{b}{2} \biggr) P_1 \\&=\biggl(\frac{\theta}{1+\theta}+ \frac{(\alpha-1) \theta}{2(1+\theta)} \biggr) \ \alpha \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \frac{\theta}{1+\theta} \\&=\frac{(\alpha+1) \alpha}{2!} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \biggl( \frac{\theta}{1+\theta} \biggr)^2 \\&=\binom{\alpha+1}{2} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \biggl( \frac{\theta}{1+\theta} \biggr)^2=P[X=2] \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+P_2%26%3D%5Cbiggl%28a%2B%5Cfrac%7Bb%7D%7B2%7D+%5Cbiggr%29+P_1+%5C%5C%26%3D%5Cbiggl%28%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D%2B+%5Cfrac%7B%28%5Calpha-1%29+%5Ctheta%7D%7B2%281%2B%5Ctheta%29%7D+%5Cbiggr%29+%5C+%5Calpha+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5C%5C%26%3D%5Cfrac%7B%28%5Calpha%2B1%29+%5Calpha%7D%7B2%21%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E2+%5C%5C%26%3D%5Cbinom%7B%5Calpha%2B1%7D%7B2%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E2%3DP%5BX%3D2%5D++%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

![\displaystyle \begin{aligned} P_3&=\biggl(a+\frac{b}{3} \biggr) P_2 \\&=\biggl(\frac{\theta}{1+\theta}+ \frac{(\alpha-1) \theta}{3(1+\theta)} \biggr) \ \frac{(\alpha+1) \alpha}{2!} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \biggl( \frac{\theta}{1+\theta} \biggr)^2 \\&=\frac{(\alpha+2) (\alpha+1) \alpha}{3!} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \biggl( \frac{\theta}{1+\theta} \biggr)^3 \\&=\binom{\alpha+2}{3} \ \biggl(\frac{1}{1+\theta} \biggr)^\alpha \ \biggl( \frac{\theta}{1+\theta} \biggr)^3=P[X=3] \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+%5Cbegin%7Baligned%7D+P_3%26%3D%5Cbiggl%28a%2B%5Cfrac%7Bb%7D%7B3%7D+%5Cbiggr%29+P_2+%5C%5C%26%3D%5Cbiggl%28%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D%2B+%5Cfrac%7B%28%5Calpha-1%29+%5Ctheta%7D%7B3%281%2B%5Ctheta%29%7D+%5Cbiggr%29+%5C+%5Cfrac%7B%28%5Calpha%2B1%29+%5Calpha%7D%7B2%21%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E2+%5C%5C%26%3D%5Cfrac%7B%28%5Calpha%2B2%29+%28%5Calpha%2B1%29+%5Calpha%7D%7B3%21%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E3+%5C%5C%26%3D%5Cbinom%7B%5Calpha%2B2%7D%7B3%7D+%5C+%5Cbiggl%28%5Cfrac%7B1%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E%5Calpha+%5C+%5Cbiggl%28+%5Cfrac%7B%5Ctheta%7D%7B1%2B%5Ctheta%7D+%5Cbiggr%29%5E3%3DP%5BX%3D3%5D++%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

The above derivation demonstrates that formula (12) generates the same probabilities as (8). By adjusting the constants

With the initial probability

More Examples

Example 3

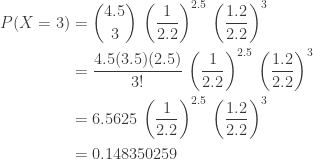

Suppose that an insured will produce

where

What is the probability that a randomly selected insured will produce more than 2 claims during the next exposure period?

Note that the claim frequency for an individual insured has a Poisson distribution with mean

The following calculation gives the relevant probabilities to answer the question.

Summing the three probabilities gives

Example 4

The number of claims in a year for each insured in a large portfolio has a Poisson distribution with mean

Determine the proportion of insureds that are expected to have less than 1 claim in a year.

Setting

Example 5

Suppose that the number of claims in a year for an insured has a Poisson distribution with mean

One thousand insureds are randomly selected and are to be observed for a year. Determine the number of selected insureds expected to have exactly 3 claims by the end of the one-year observed period.

With this being a Poisson-gamma mixture, the number of claims in a year for a randomly selected insured has a negative binomial distribution. Using (8) and based on the gamma parameters given, the following is the probability function of negative binomial distribution.

The following gives the calculation for

With

Example 6

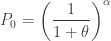

Suppose that the annual claims frequency for an insured in a large portfolio of insureds has a distribution that is in the (a,b,0) class. Let

Given that

Given

Solving these two equations gives

Dan Ma actuarial

Daniel Ma actuarial

Dan Ma math

Dan Ma mathematics

Revised Nov 2, 2018.

Pingback: Practice Problem Set 6 – Negative Binomial Distribution « Practice Problems in Actuarial Modeling

Pingback: The big 3 claim frequency models | Topics in Actuarial Modeling

Pingback: Negative binomial distribution – A World of Ideas

Many thanks for your fantastic post on Negative Binomial Distribution. Which material of actuarial has this topic covered in more details? Is it CT3 or CT6. Could you suggest a book covering the topics in your blog, please?